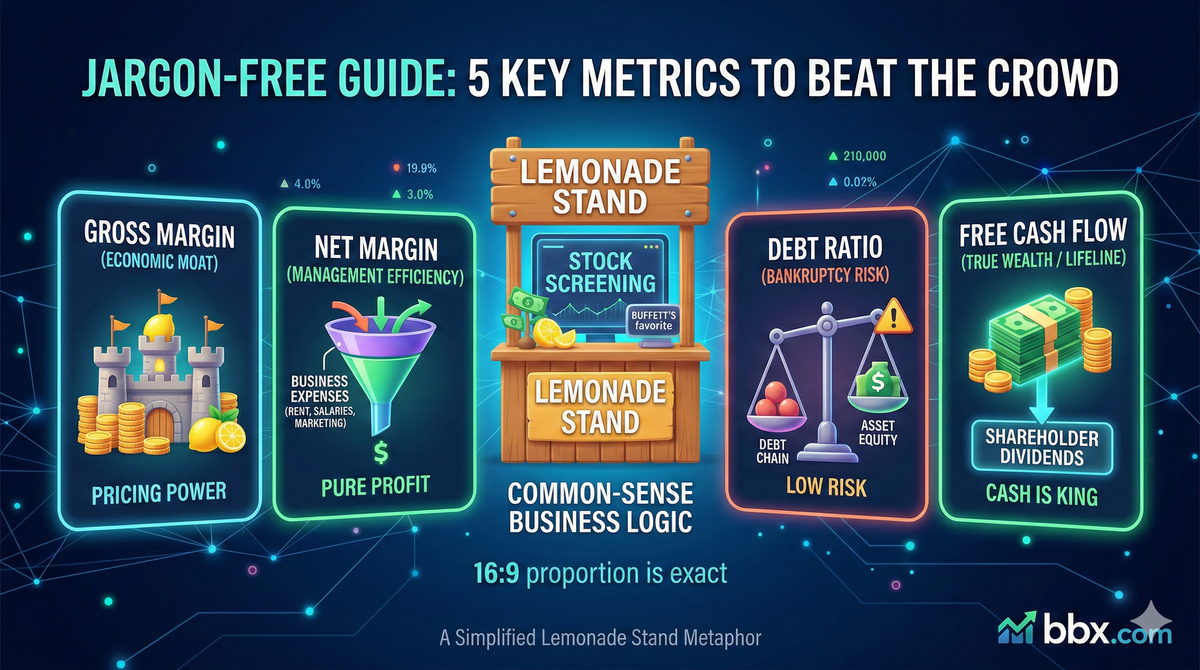

5 Common-Sense Financial Metrics to Beat 80% of Retail Investors

What are the best financial metrics for stock picking? Learn to evaluate Gross Margin, Net Margin, ROE, Debt Ratio, and FCF without complex math on bbx.com.

TL;DR : Retail investors lose money because they treat the stock market like a casino, relying on rumors and guessing games. True investing is allocating capital to great businesses that make money effortlessly and have clean balance sheets. Forget the complex accounting formulas. When screening stocks on bbx.com, you only need to evaluate a company like you would a neighborhood "Lemonade Stand" by asking 5 common-sense questions:Gross Margin: Can you charge a premium price? (Measures your Economic Moat)Net Margin: What’s actually left in the register after expenses? (Measures Management Efficiency)ROE: How fast does the shareholders' money compound? (Measures Earning Power - Buffett's favorite)Debt Ratio: How much money do you owe the bank? (Measures Bankruptcy Risk)Free Cash Flow (FCF): How much cold, hard cash is available for dividends? (Measures the True Bottom Line)

Introduction: Buying a Stock Means Buying a Business

Many people open their trading apps, see a dense wall of financial data, and immediately feel dizzy. The truth is, you absolutely do not need to be a Certified Public Accountant (CPA) to be a phenomenal investor.

If investing in a stock is like buying a racecar, Technical Analysis helps you gauge the wind direction on the track, while Fundamental Analysis is how you pop the hood to check if the engine is powerful and the chassis is sturdy.

Today, we are throwing away all the mathematical formulas. We will continue to use our "BBX Lemonade Stand" analogy to explain the 5 core yardsticks of stock picking using everyday business logic.

Yardstick 1: Gross Margin — How Strong is Your "Pricing Power"?

Why does a street vendor barely scrape by making pennies, while a brand like Starbucks rakes in massive profits selling the exact same beverage? The secret lies in Gross Margin.

- The Common-Sense Translation: You sell a cup of lemonade for $20. Buying the lemons, tea, and cups cost you $5. The remaining $15 is your Gross Profit. Gross Margin measures how much revenue you retain after deducting the absolute basic costs of making your product.

- The BBX Reality Check: Gross Margin represents a product's "Irreplaceability" and the company's "Economic Moat." If a company consistently boasts a Gross Margin of 60% or even 80% (think Apple's iPhone, luxury brands, or high-end software), it means consumers are willing to pay a massive premium for its brand or technology. When inflation hits and lemon prices soar, high-margin companies can simply raise their prices to survive. Conversely, companies with razor-thin margins survive purely on brutal "price wars" and have virtually zero resistance to economic risks.

Yardstick 2: Net Margin — Is Your Management Burning Cash?

Just because you have a high Gross Margin doesn't mean you are getting rich. Many viral popup stores have lines out the door, yet go bankrupt by the end of the year. Why? Because they are bleeding money elsewhere.

- The Common-Sense Translation: That $15 of Gross Profit doesn't go straight into your pocket. You have to pay exorbitant storefront rent, hire expensive social media influencers, pay your store manager a high salary, and pay taxes. After stripping away all of these expenses, the actual money left in your savings account is your Net Income.

- The BBX Reality Check: Net Margin measures the management team's "Operational Efficiency" (i.e., how good they are at not wasting money). Some companies have fantastic Gross Margins, but pitiful Net Margins. This means management is burning cash—either marketing expenses have spiraled out of control, or executives are paying themselves absurd salaries. A true winning stock needs a product that sells at a premium (High Gross Margin) AND a management team that keeps that money safely inside the company (High Net Margin).

Yardstick 3: ROE (Return on Equity) — Warren Buffett's "Money Printer"

If the legendary Warren Buffett could only look at a single metric to pick a stock, he would choose ROE. It directly answers the most critical question a shareholder can ask: If I give you my capital, what interest rate will you generate for me this year?

- The Common-Sense Translation: You invested $100,000 of your own hard-earned money (Equity) to open this lemonade stand. After a year of hard work, you netted $20,000 in pure profit. Your ROE is 20%. That means your investment yielded an annualized return of 20%—vastly outperforming any savings account or CD!

- The BBX Reality Check: ROE measures the ultimate efficiency of a business's ability to "compound capital." There is an unwritten rule on Wall Street: A company that consistently maintains an ROE above 15% for multiple years is typically a premium business with a long-term competitive advantage. If a company's ROE sits at 3% or is negative year after year, you are better off buying risk-free Treasury bonds than investing in their stock.

Yardstick 4: Debt Ratio — Will the Chassis Snap in a Storm?

Borrowing money to run a business isn't shameful; leverage helps you open branch stores faster. But if you borrow too much, the slightest market turbulence will capsize your ship.

- The Common-Sense Translation: It takes $1,000,000 to open a luxury flagship lemonade stand. You only have $200,000 in your pocket. The remaining $800,000 is borrowed from the bank. Your Debt Ratio is 80%.

- The BBX Reality Check: The Debt Ratio is the "Sword of Damocles" hanging over a company's head. During an economic boom with low interest rates, leveraging up feels amazing. But if the Federal Reserve aggressively hikes interest rates, or a recession hits (and people stop buying $20 lemonade), crushing interest payments will instantly bleed you dry, leading to a liquidity crisis and bankruptcy. For standard, non-financial companies, look for Debt Ratios under 50% so you can sleep soundly at night.

Yardstick 5: Free Cash Flow (FCF) — The "Cold, Hard Cash" for You

Finally, we must return to the coldest reality of business: making a profit is one thing; having the cash available to distribute to owners is an entirely different story.

- The Common-Sense Translation: At year-end, your accounting books show you netted $100,000 in cash. However, your commercial ice machine broke down. To keep the doors open next year, you are forced to spend $30,000 on new equipment (Capital Expenditures, or CapEx). The remaining **$70,000** is the money you can freely use to pay yourself a dividend or buy a sports car. This is your Free Cash Flow.

- The BBX Reality Check: Free Cash Flow is the truest measure of a company's actual wealth. If a company claims to be highly profitable every year, but its Free Cash Flow is consistently negative, it is a "cash incinerator." It must constantly borrow money or issue new shares just to maintain its operations. Truly great companies (like Apple or Microsoft) generate so much Free Cash Flow they don't know what to do with it. This gives them the power to aggressively buy back their own stock during bear markets (boosting your share price) or reward you with juicy cash dividends.

Interactive Case Study: Spot the "Impostor" Using Common Sense

Now, use your newly acquired business common sense to uncover the true colors of two rival companies in the same industry:

| Metric | Company A (Seemingly Fierce) | Company B (Low-Profile Cash Cow) |

| Gross Margin | 15% (Survives on discounts) | 55% (Premium brand, sells easily) |

| ROE | 25% (Looks extremely tempting) | 20% (Highly robust) |

| Debt Ratio | 85% (Drowning in debt) | 30% (Thick financial cushion) |

| Free Cash Flow | Negative for 3 consecutive years | Billions in positive inflow annually |

[BBX Expert Analysis]: Many retail investors will take one look at Company A's 25% ROE and blindly buy in! But apply common-sense logic: Company A's product has zero competitive advantage (low Gross Margin). The only reason its ROE is high is because it is a "Gambler"—it engineered that return by maxing out its leverage with an 85% Debt Ratio. The moment banks call in the loans or interest rates rise, Company A will go bankrupt. Furthermore, it has no Free Cash Flow to reward you.

On the other hand, Company B commands a premium price (High Gross Margin), owes very little to the banks (Low Debt), and generates mountains of cold, hard cash that it can distribute to shareholders. In the investing world, always bet your money on a low-profile cash machine like Company B!

Disclaimer: This report is for informational purposes only and does not constitute financial advice.