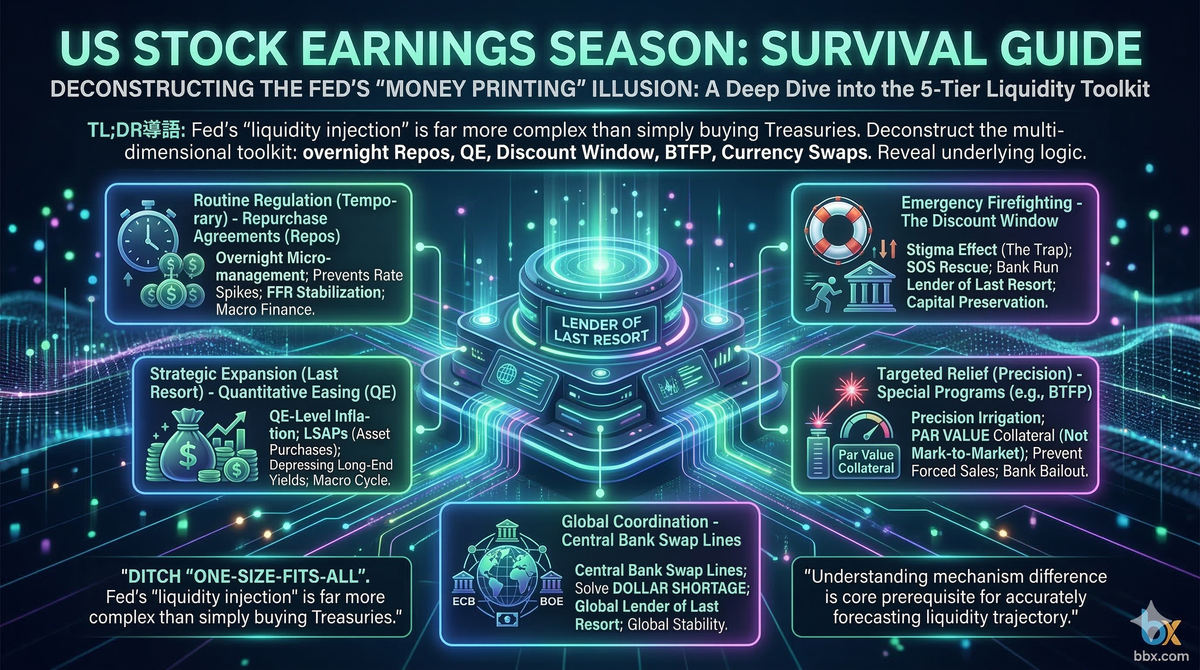

Mapping the Liquidity Crisis Response: A Deep Dive into the Fed's 5-Tier "Injection" Toolkit

The Fed's "liquidity injection" is far more complex than simply buying Treasuries. We deconstruct the Federal Reserve's multi-dimensional toolkit—from overnight Repos and QE to the Discount Window, BTFP, and Currency Swaps—revealing the underlying logic of macro-financial interventions.

TL;DR (Core Summary): In the modern fiat monetary system, the central bank plays the critical role of the "Lender of Last Resort." The public often oversimplifies the Federal Reserve's balance sheet expansion as mere "money printing," but this is a gross misconception. In reality, based on the urgency of the financial stress, the duration of the intervention, and the target audience, the Fed deploys a highly structured liquidity injection toolkit. This article distills these complex interventions into five distinct tiers: from daily fine-tuning via Repurchase Agreements (Repos) to macro-cycle-altering Quantitative Easing (QE); from the ultimate backstop of the Discount Window to surgical crisis-management tools like the Bank Term Funding Program (BTFP), and finally, global stabilization via Currency Swaps.

Introduction: Beyond the "Asset Purchase" Monolith

When the macroeconomy experiences violent swings or the financial system faces a liquidity drought, the Fed's policy response is rarely a monolithic action like "buying short-term T-Bills in the open market." The transmission mechanism of monetary policy requires the central bank to possess multi-dimensional intervention capabilities.

To accurately anchor interest rates and preempt systemic risk, the Fed's intervention tools can be categorized into the following five core tiers based on their level of normalization and targeting precision.

Tier 1: Routine Fine-Tuning — Repurchase Agreements (Repo Operations)

This is the Fed's Fine-Tuning Operation for daily liquidity management, representing its most frequent "micro-management" tool.

- The Mechanism: Through Open Market Operations (OMO), the Fed engages in short-term borrowing and lending with Primary Dealers. In a standard Repo operation, the Fed injects cash into the market, and dealers pledge High-Quality Liquid Assets (HQLA)—such as U.S. Treasuries or Agency debt—as collateral. They agree to repurchase these assets with interest after a very short period (usually overnight or up to a couple of weeks).

- Policy Nature: Temporary and high-frequency. This injection acts as a short-term "lubricant" for the interbank lending market. Once the operation matures, the liquidity is automatically drained back out. Its core objective is to precisely anchor the Federal Funds Rate (FFR) within its target range, preventing anomalous liquidity crunches or gluts in the short-term funding markets.

Tier 2: Strategic Expansion — Quantitative Easing (QE)

When traditional interest rate tools hit the Zero Lower Bound (ZLB), the Fed deploys this structural balance sheet expansion tool, colloquially known by the market as the "money printer."

- The Mechanism: Unlike the temporary "borrowing" nature of Repo operations, Large-Scale Asset Purchases (LSAPs) involve outright buys. The Fed purchases massive quantities of Long-term Treasuries and Mortgage-Backed Securities (MBS) in the secondary market.

- Policy Nature: Massive scale and profound duration. Once purchased, these colossal asset portfolios sit on the Fed's balance sheet for years. The macroeconomic intent is to extract safe, long-term assets from the market, directly depressing long-end yields (flattening the yield curve). This forces investors further out the risk curve (into equities and corporate bonds), thereby outputting trillions in structural liquidity to the broader financial system to stimulate credit expansion in the real economy.

Tier 3: Emergency Firefighting — The Discount Window

As the Fed's oldest traditional tool, the Discount Window serves as the absolute Last Resort Facility for the liquidity management of U.S. commercial banks.

- The Mechanism: When a depository institution faces a sudden bank run, severe liquidity constraints, and cannot secure funding in the interbank market due to credit friction, it can apply directly to its regional Federal Reserve Bank for Primary Credit (i.e., a Discount Window loan).

- Policy Nature: Carries a strong "Emergency SOS" connotation. Historically, because borrowing emergency funds from the central bank signals to the market and peers that a bank is on the brink of insolvency, it carries a severe Stigma Effect. Banks actively avoid using it. However, during the eruption of Systemic Risk (such as the 2008 Subprime Mortgage Crisis or the 2023 Silicon Valley Bank collapse), Discount Window usage typically experiences a massive, impulsive spike, acting as the final circuit breaker to halt market panic.

Tier 4: Targeted Relief — Term Funding Programs (Special Facilities)

To address structural vulnerabilities exposed during specific crises, the Fed bypasses traditional tools to create highly targeted, temporary liquidity facilities (Special Purpose Vehicles/Facilities).

- The Mechanism & Classic Case: A prime example is the Bank Term Funding Program (BTFP) launched during the 2023 regional banking crisis. This tool allowed banks to pledge eligible assets (like U.S. Treasuries and MBS) in exchange for loans with terms of up to one year.

- The Disruptive Innovation: The core professional design of the BTFP was that collateral was valued at Par Value (face value), rather than at the heavily discounted Mark-to-Market prices caused by the Fed's aggressive rate hike cycle.

- Policy Nature: Precision irrigation / Surgical strike. This brilliantly neutralized the threat of unrealized paper losses destroying a bank's liquidity. It allowed the Fed to surgically defuse bank runs at specifically stressed institutions without having to launch broad-based QE (which would have exacerbated inflation).

Tier 5: International Coordination — Central Bank Liquidity Swaps

In the context of financial globalization and dollar hegemony, the depletion of U.S. dollar liquidity can easily trigger a transnational financial tsunami. This tool serves as the global systemic stabilization mechanism.

- The Mechanism: The Fed establishes Bilateral Swap Lines with major global central banks, including the European Central Bank (ECB), Bank of Japan (BOJ), and Bank of England (BOE). During a crisis, the Fed lends U.S. dollars to foreign central banks at a fixed exchange rate. These foreign central banks then inject this Offshore Liquidity into their domestic commercial banking systems. Upon maturity, the two parties swap their respective currencies back and pay interest.

- Policy Nature: The transnational "Global Lender of Last Resort." Through this coordinated international operation, the Fed effectively alleviates sudden "Dollar Shortages" in overseas markets, ensuring that global trade settlements, supply chain financing, and cross-border asset pricing systems do not paralyze due to a lack of dollars.

Conclusion

The Federal Reserve's open market operations are far from a simple binary of "turning the liquidity taps on or off." From Repo operations that soothe daily interest rate volatility to Quantitative Easing that reshapes the macroeconomic cycle; from targeted programs like the BTFP that save regional banks from runs, to the Liquidity Swaps that stabilize the global financial network.

These five tools intertwine across durations, underlying assets, pricing mechanisms, and target audiences to forge a formidable defense line for the modern dollar system against economic cycles. For professional investors, understanding the hierarchical and mechanical differences of these tools is the core prerequisite for accurately forecasting the trajectory of macro-financial liquidity.

Disclaimer: This report is for informational purposes only and does not constitute financial advice.