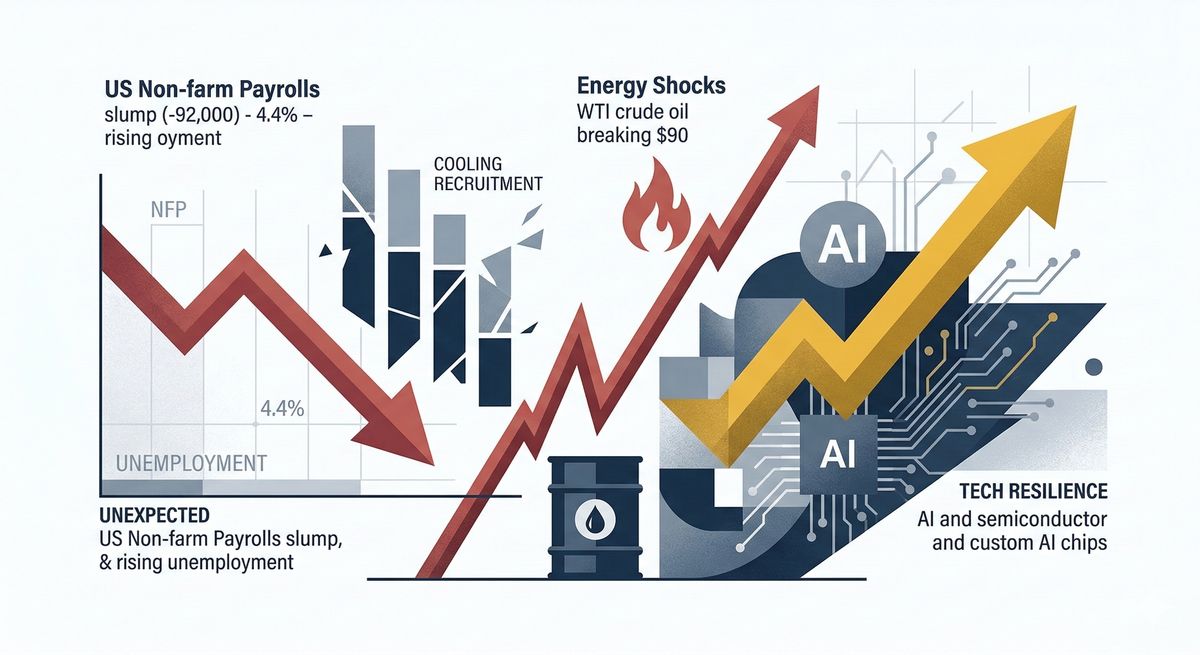

March 6th Market Watch: Macro Turbulence, Energy Shocks, and the Structural Shift in Tech

US NFP plummeted by 92,000, signaling a labor chill as unemployment hit 4.4%. With WTI oil breaching $90 amid Iran-US tensions, and Marvell (MRVL) surging 18% on AI demand, explore why institutional investors are pivoting to complex hedging and tech alpha.

How does the unexpected NFP slump and the $90 oil spike redefine the 2026 investment landscape? As US unemployment climbs to 4.4% and geopolitical tensions in the Middle East threaten global supply chains, institutional investors are pivoting from growth-only strategies to complex hedging. Explore the definitive analysis of the March 6th market volatility.

1. Macro Breakdown: The NFP "Ice Age" and Fed Pivot Odds

The labor market data released on March 6th sent shockwaves through the financial sector. US Non-farm Payrolls (NFP) for February plummeted by 92,000—a stark contrast to the anticipated 55,000 gain. This represents one of the most significant misses in recent cycles, partly driven by healthcare strikes and a cooling recruitment appetite in the tech and AI sectors.

- Unemployment & Consumption: The unemployment rate ticked up to 4.4%, surpassing both expectations and the previous 4.3%. More concerning is the retail data; January retail sales saw a 0.2% month-on-month decline, the first negative growth since last October, signaling that the American consumer engine may be losing steam.

- Monetary Policy Implications: The market has rapidly priced in a more dovish Federal Reserve. The probability of a June rate cut has surged to 37.6% (up from 30% prior to the data). However, Wall Street remains cautious, with Goldman Sachs maintaining that the Fed needs to see consecutive months of labor weakness before committing to a full normalization of real interest rates.

2. Energy and Geopolitics: The $100 Oil Shadow

While the Fed grapples with labor data, the energy market is facing a "Black Swan" event. WTI crude oil breached the $90 mark, recording its largest single-week percentage gain since 1983.

- The Iranian Factor: Tensions escalated following reports of attacks on US-affiliated tankers near Kuwait. With the White House adopting a hardened stance—demanding unconditional surrender from Tehran—the prospect of a protracted conflict is now a baseline scenario.

- Supply Chain Chokepoint: If the Strait of Hormuz faces even a partial blockade in the coming weeks, energy analysts warn of a rapid spike toward $100 or $110 per barrel. This "Energy-Push Inflation" creates a nightmare scenario for the Fed: slowing growth coupled with rising costs (Stagflation).

3. Structural Divergence: Tech Resilience vs. Credit Fragility

Despite the macro gloom, a massive divergence is appearing between the "New Economy" (AI/Semiconductors) and the "Debt Economy" (Private Credit).

- The AI Alpha: Marvell Technology (MRVL) provided a masterclass in resilience, surging over 18% post-earnings. Their Q4 revenue hit a record $2.22 billion, driven by an insatiable demand for custom AI chips. This confirms that while the broader economy slows, the AI infrastructure build-out remains decoupled from typical cycle constraints.

- Credit Cracks: On the flip side, the private credit market is showing signs of stress. Blue Owl Capital and other major asset managers have begun restricting redemptions in certain credit funds following exposure to London-based real estate defaults. This liquidity tightening suggests that the "higher for longer" era is finally breaking the weakest links in the global credit chain.

4. Technical Outlook: The VIX and the 6,700 Support

From a technical perspective, the S&P 500 continues to find a floor near the 6,700 level. Although the VIX (Volatility Index) has spiked toward 30—the highest level in months—institutional flow data shows that this is largely driven by "insurance buying" (hedging via options) rather than panic selling.

If geopolitical tensions stabilize over the weekend, we expect a technical rebound as institutional hedges are unwound. However, a breach of the 6,700 support combined with a VIX surge above 35 would signal a transition into a deeper corrective phase, requiring a radical reassessment of risk parity portfolios.