Revering the Unknown: Institutional Defenses Against "Black Swans" and Extreme Tail Risk

Think a hard stop-loss guarantees your safety? Uncover the lethal traps of overnight gap-downs and extreme slippage. Learn to build an "antifragile" portfolio through strict exposure limits and correlation decoupling to survive unpredictable Black Swan events.

TL;DR (Core Summary): In the trading arena, the greatest risk is always what you "don't know that you don't know."The Illusion of the Hard Stop: A stop-loss order is not a magical forcefield. During extreme liquidity vacuums or overnight gap-downs, your stop order will be bypassed entirely (Slippage), resulting in realized losses far exceeding your planned 2%.Tail Risk: Events that are statistically highly improbable but carry catastrophic, systemic consequences when they do occur (commonly known as "Black Swans").The Antifragile Framework: Institutions do not defend against Black Swans by predicting them; they do so by reducing systemic fragility. Implementing Total Exposure Limits, isolating asset correlation, and treating cash as an active position are the only ways to survive the market's darkest hours.

Introduction: When Your "Perfect Stop-Loss" Becomes Useless

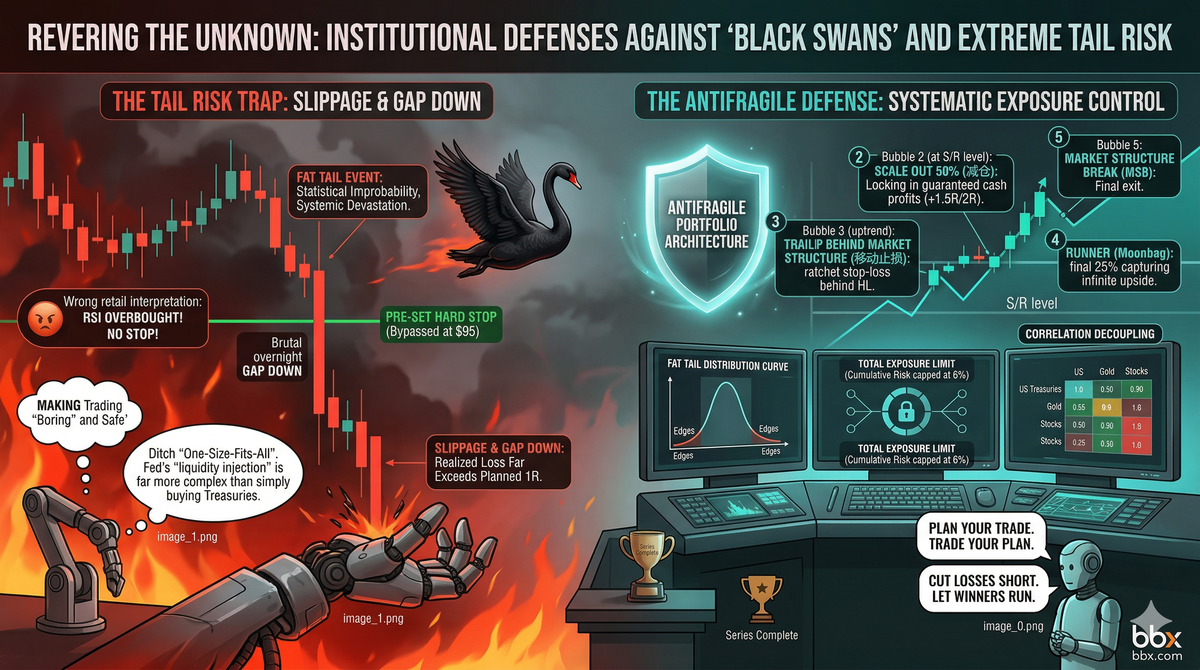

Imagine this scenario: After rigorous analysis, you buy an asset at $100 and set a hard stop-loss at $95, strictly adhering to the 2% single-trade risk rule. You close your laptop, thinking, "The absolute worst-case scenario is a 2% loss. I am completely safe."

However, over the weekend, an unprecedented geopolitical conflict erupts, or a macroeconomic behemoth unexpectedly files for bankruptcy. When the market opens on Monday morning, the price doesn't even pause at $95. It opens violently at $70. Your stop-loss (which functions as a stop-market order) is triggered at the open and executes at the best available price in the order book—which is $70. You planned to lose $5, but you ultimately lost $30. If you were using even a moderate amount of leverage, this Gap Down and the resulting severe Slippage could instantly wipe out your entire account equity, or worse, leave you owing the brokerage money.

This is the most chilling reality of the financial markets: Technical analysis cannot predict Black Swans, and standard stop-loss orders cannot defend against a total collapse of liquidity.

I. Meeting the Reaper: Tail Risk and Black Swans

In financial statistics, the distribution of market returns does not form a perfect, symmetrical bell curve; it exhibits "Fat Tails."

- The Normal Market (The Belly of the Curve): Daily fluctuations of 1% to 3%. This is where technical analysis and conventional risk management thrive.

- Tail Risk (The Extremes of the Curve): These are extreme events whose probability of occurrence lies in the absolute margins (e.g., beyond -3 standard deviations) but possess devastating destructive power. Examples include the 2008 Lehman Brothers collapse, the 2015 Swiss Franc shock, and the 2020 pandemic-induced global market meltdowns.

Nassim Nicholas Taleb, author of The Black Swan, emphasizes that Black Swan events are highly unpredictable, carry massive impact, and are often rationalized by hindsight bias. The most foolish endeavor a retail trader can undertake is obsessively watching the news to "predict" the next Black Swan. Elite risk managers understand a fundamental truth: Since these events are unpredictable, our only mandate is to ensure we are not standing at ground zero when the explosion occurs.

II. Institutional Defense: Building an "Antifragile" System

How do you survive an unpredictable catastrophe? You must elevate your focus from micro "single-trade risk management" to macro "Portfolio and Exposure Management."

1. Strict Total Exposure Limits

Adhering to the 2% rule on a single trade is insufficient. If you simultaneously hold 10 long positions, each risking 2%, your true portfolio risk during a macro Black Swan is actually 20% or higher, as all assets will likely plummet simultaneously. The Institutional Rule: Establish a "Maximum Correlated Risk Limit." For example, at any given moment, the cumulative potential loss of all open positions combined must absolutely never exceed 6% or 10% of total account equity. Once you hit this cap, you are prohibited from opening new risk-on positions.

2. Beware the Correlation Trap

You might think you are diversified: you bought tech stocks, cryptocurrencies, and an S&P 500 ETF. During peacetime, their price actions might differ. But during the sheer panic of a Black Swan, the correlation of all risk assets converges to 1. Every market participant ruthlessly liquidates assets in a desperate dash for cash. Your "diversification" instantly morphs into a massive, concentrated, single-directional bet. The Institutional Rule: True diversification requires allocating capital to assets that are fundamentally decoupled or negatively correlated (e.g., holding U.S. Treasuries or Gold as a ballast), or actively utilizing options to construct tail-risk hedges.

3. Cash is an Active Position

Many novice traders suffer from "idle cash anxiety"—if there is purchasing power in their account, they feel a compulsive need to deploy it, as if holding cash is a missed opportunity. The Institutional Rule: Cash is the ultimate, flawless hedge against Tail Risk. Furthermore, it is the only "dry powder" that allows you to step in and buy "blood in the streets" at generational discounts while over-leveraged participants are being forcibly liquidated. Never be 100% invested. Maintaining ample liquidity reserves is the cornerstone of an Antifragile portfolio.

Conclusion: Revere the Market to Survive It

Trading, stripped to its core, is a game of survival.

Those arrogant "trading prodigies" who utilize 100x leverage during a raging bull market typically vanish into obscurity after a single Black Swan event. The true veterans—the evergreen traders who survive and compound wealth over decades—all share a profound reverence for the market's destructive capabilities.

Do not attempt to be the oracle who predicts the hurricane. Instead, focus entirely on building a ship sturdy enough to weather the storm. When you ruthlessly control your exposure, decouple your correlations, and hold ample cash reserves, you can dust yourself off after the darkest Black Swan and calmly return to the trading desk.

Disclaimer: This report is for informational purposes only and does not constitute financial advice.