The "Lie Detector" of Earnings Reports: Why High Net Income Doesn't Mean a Great Company

A company reports a massive $100M profit, yet its stock crashes or it faces bankruptcy. Why? Learn to spot the "Accrual Accounting" illusion and "One-off Asset Sales" trap. Master Operating Cash Flow (OCF) to avoid stock market fraud on bbx.com.

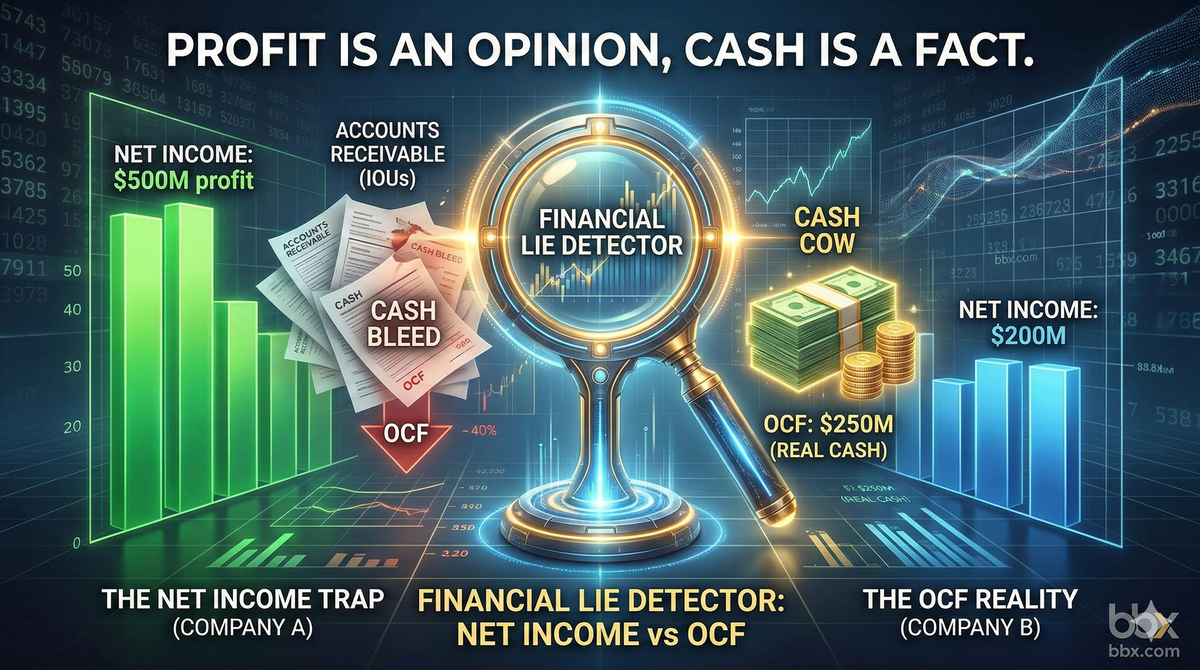

TL;DR (Quick Answer): In the ruthless world of capital markets, every professional trader lives by one absolute rule: "Profit is an opinion, Cash is a fact." Never go all-in just because an earnings report screams "Net Income Surges 200%!" Behind sky-high profits often lie two deadly traps that can bankrupt a company overnight:Trap 1 (Profit vs. Cash): A company earns $100 million on paper, but it's entirely composed of customer IOUs (Accounts Receivable). The company doesn't even have the cash to make next month's payroll. The Fix: Ruthlessly track Operating Cash Flow (OCF).Trap 2 (Core Business vs. Financial Gymnastics): Profits surged not because the core product is selling well, but because the company sold a building or received a government subsidy (Non-recurring Items). The Fix: Strip out one-off gains and scrutinize Non-GAAP Net Income.

Introduction: Puncturing the Glamorous Bubble of "Net Income"

In our previous guide, The Big Three Financial Statements, we established a macro concept: The Income Statement is the "Report Card," the Balance Sheet is the "Foundation," and the Cash Flow Statement is the "Lifeline."

The vast majority of novice investors only look at one number at the very bottom of the Income Statement—Net Income (The Bottom Line). They naively assume that as long as the profit is positive and growing year-over-year, it must be an exceptional company to invest in. Shortly after they buy in, the company suddenly announces a liquidity crisis, and the stock goes to zero.

Why does this seemingly contradictory phenomenon occur? Because the underlying logic of modern business is built on Accrual Accounting. Simply put, a company can legally and compliantly "manufacture" staggering profits on its books without a single dime of actual cash entering its bank accounts.

Today, we will venture into the dark corners of earnings reports, deconstruct the two traps that wipe out countless retail investors, and hand you two professional-grade "lie detectors."

Trap 1: Paper Wealth Hijacked by "Accounts Receivable"

Let's return to our familiar BBX Lemonade Stand.

Assume this year, your stand scores a massive corporate order: A major tech giant orders $100 million worth of lemonade as an annual employee perk. The tea is brewed and successfully delivered. Because your cost of goods was only $20 million, on the day of delivery, your Income Statement legally and compliantly records a massive **$80 million in Net Income**.

The moment the earnings report drops, retail investors go wild and scramble to buy your stock. However, the cruel reality of the script is this: The tech giant informs you that, per industry standard, this $100 million invoice will be paid on Net-180 terms (paid 180 days later).

- The Illusion (Paper Wealth): Your Net Income shines brilliantly at $80 million.

- The Hidden Danger (The Foundation): On your Balance Sheet, that $100 million turns into an extremely dangerous line item—Accounts Receivable. In plain English: a massive pile of IOUs.

- The Crisis (The Lifeline): Next week, you need to pay your lemon suppliers, store rent, and employee payroll. You look at a drawer full of IOUs, but you can't scrape together a single dollar in cash. Ultimately, this "star company" that made $80 million on paper files for bankruptcy due to a Liquidity Crisis.

Lie Detector 1: Operating Cash Flow (OCF)

To avoid being fooled by "IOU Profits," professional analysts flip straight to the Cash Flow Statement and lock their eyes on Operating Cash Flow (OCF).

- Core Definition: It represents the cold, hard cash a company actually collected purely from running its core business. It strips out all unpaid IOUs and non-cash expenses (like depreciation).

- The Wall Street Rule: The ultimate standard for testing a company's "Earnings Quality" is the ratio of OCF to Net Income.

- If a company's Net Income grows rapidly for consecutive years, but its OCF is persistently negative or drastically lower than Net Income, this is a DEFCON 1 red flag! It means its profits are built entirely on aggressive credit sales or outright financial fraud (e.g., the infamous early Luckin Coffee scandal).

- True cash-printing machines (like Apple or Microsoft) usually boast an OCF that is consistently greater than or equal to their Net Income.

Trap 2: The Financial Facelift of "Selling the Farm"

Let's look at the second trap. Suppose the actual business of the BBX Lemonade Stand is abysmal this year. Selling tea didn't make a dime; in fact, the core business lost $10 million.

To make the year-end earnings look pretty and artificially prop up the stock price, management makes a decision: Sell a vacant downtown storefront the company bought ten years ago for a premium of $50 million. When the year-end report is published, the money made from selling the real estate covers the operational losses, and total profit magically becomes +$40 million!

A novice reading the headlines will gasp, "Wow, this lemonade stand netted $40 million this year! Incredible performance!" But anyone with basic business acumen knows the intrinsic value of this $40 million is effectively zero.

Lie Detector 2: Net Income Excluding Non-recurring Items (Non-GAAP)

Profits from selling real estate, divesting subsidiaries, stock market gains, or receiving one-off government tax subsidies are collectively categorized in accounting as Non-recurring Items or One-off Gains. As the name implies, this is money falling from the sky—it will not happen again next year.

- Core Definition: To evaluate a company's true ability to generate wealth, you must ruthlessly strip away these "one-off windfalls." You need to see exactly how much money it made purely from selling its core products (whether that's lemonade, software, or electric vehicles). This metric is often referred to as Operating Profit or Non-GAAP Net Income.

- The Wall Street Rule: If a company loses money on its core operations year after year, and relies entirely on "selling the farm" or financial gymnastics to maintain a marginal paper profit (often just to avoid getting delisted), its true colors will be exposed the moment it runs out of assets to sell. Refuse to invest in any company whose core business cannot turn a profit!

Interactive Case Study: Catching the Impostors

Now, apply your two newly acquired "lie detectors" to examine the core financial metrics of the following two companies (Figures in USD Millions):

| Core Financial Metric | Company A (Seemingly Glamorous) | Company B (Seemingly Average) |

| Net Income | $500 | $200 |

| Increase in Accounts Receivable | **$600** (Aggressive Credit Sales) | $10 |

| Operating Cash Flow (OCF) | **-$100** (Severe Cash Bleed) | $250 (Cash Cow) |

| Non-recurring Gains | $450 (Sold HQ Building) | $0 |

If you were a professional trader at BBX, which company would you trust with your capital?

[BBX Expert Analysis]: Avoid Company A at all costs! Even though Company A boasts a massive $500 million in Net Income, it is a mirage on the verge of collapse. First, $450 million of that profit came from selling a building (Non-recurring Item), meaning its core business has essentially lost its ability to generate profit. Second, its Accounts Receivable exploded abnormally, resulting in a negative Operating Cash Flow (-$100M) after a full year of hard work. Not only did it fail to make real money, but it is also actively draining the company's liquidity.

Conversely, Company B only reported $200 million in Net Income, but that $200 million has zero fluff (Non-recurring gains are $0). More impressively, its Operating Cash Flow is a robust $250 million. This is a remarkably healthy business with immense pricing power over its clients (it doesn't need to offer IOUs to make sales). In the realm of value investing, you always buy Company B!

Disclaimer: This report is for informational purposes only and does not constitute financial advice.