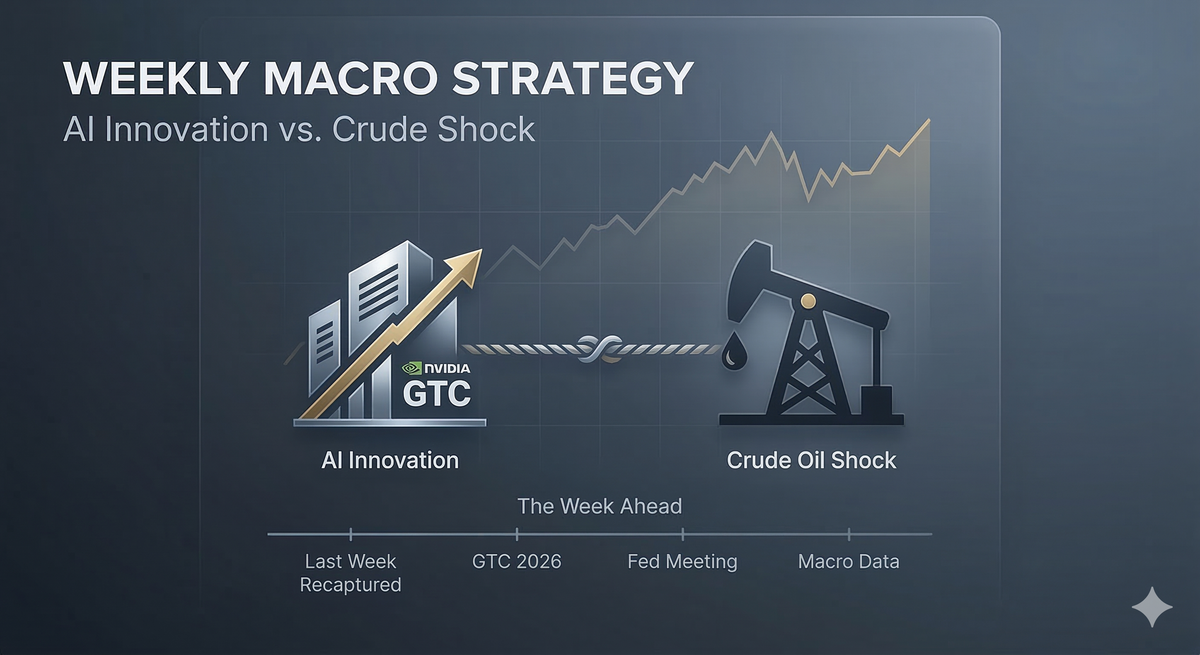

Weekly Macro Strategy: From the Crude Oil Shock to NVIDIA’s GTC "Moment of Truth"

Last week’s rally was hijacked by a crude oil surge, forcing the "Magnificent Seven" into a technical correction. As we pivot to a high-stakes week, can NVIDIA’s GTC 2026 innovation outpace the macro shadow of the Fed's dot plot? A deep dive into last week's shock and a roadmap for the week ahead.

Recapping a volatile week of technical corrections and previewing the 2026 Central Bank Super Week.

"After a week that redefined market risk, we are moving from the 'AI Gospel' script to a complex game of geopolitical chess. Last week, the sudden resurgence of crude oil didn't just push up prices; it throttled the Nasdaq's momentum, forcing the 'Magnificent Seven' into a technical correction. As we look ahead to the next five trading days, the focus shifts from last week's shock to this week's survival: NVIDIA’s GTC showcase must now compete with a high-stakes Fed meeting and a global central bank 'Super Week.' Here is the essential bridge between where we were and where we are heading."

I. Retrospective: The "Black Gold" Stranglehold

Last week marked a significant pivot in market narrative. The optimism surrounding the Trump administration’s potential easing of chip export bans was eclipsed by the "Black Swan" in the Middle East.

- The Transmission Chain: We witnessed a brutal chain reaction: rising crude oil $\rightarrow$ surging inflation expectations $\rightarrow$ higher 10-year Treasury yields $\rightarrow$ downward pressure on tech valuations.

- Technical Correction: The "Magnificent Seven" index closed roughly 10% below its October highs, officially entering a technical correction. The market is no longer trading purely on AI potential; it is trading on energy-driven liquidity constraints.

- Crude vs. Silicon: For much of the week, the Nasdaq’s movement was inversely correlated with WTI Crude. The core conflict is clear: Energy costs are now the primary bottleneck for the AI revolution.

II. The Week Ahead: Three Critical Fronts

1. NVIDIA GTC 2026: The "AI Gospel" Returns

NVIDIA’s flagship event (March 16–19) is the bull's strongest defense.

- The Historical Edge: NVIDIA has an 80% probability of rising during GTC, with an average gain of 6%.

- What to Watch: Beyond the next-gen architecture, keep a close eye on AI Agents and software ecosystem expansion. The market is shifting its focus from "Training" to "ROI"—investors want to see how these multi-billion dollar CapEx spends will generate quantifiable revenue in the next few quarters.

2. The Central Bank "Super Week" & The Powell Standoff

The Fed meeting headlines a week of intense central bank activity (including the UK, Japan, and the Eurozone).

- The Dot Plot Bomb: While keeping rates unchanged is the consensus (92% probability), the real danger lies in the "Dot Plot." Any hawkish shift—suggesting fewer cuts or even discussing a hike—could be catastrophic for growth stocks.

- Political Friction: Jerome Powell is navigating a "judicial-political" entanglement with the Trump administration. His hinted intent to stay on the Board of Governors until 2028 serves as a signal of institutional independence, but it risks a "frozen" relationship with the White House that could cloud future policy communication.

3. Macro Data: CPI and the Manufacturing Pulse

Inflation remains "sticky." After January’s core CPI hit 3.6%, the market is looking at the February data for signs of stabilization.

- CPI Outlook: The consensus expects a headline rate around 2.9%. If the data exceeds this, expect the dollar to strengthen and bond markets to sell off further.

- Employment: Initial jobless claims remain steady (210k–213k), reflecting a resilient labor market that gives the Fed more room to remain hawkish for longer.

III. Strategy: Defensive Growth or Discount Hunting?

As we move into this "Triple-Threat" week, the core tension lies between Technological Utopia and Macro Reality.

- Valuation Check: Large-cap tech earnings yields are beginning to converge with Treasury yields. For institutional funds seeking a "safe haven," these companies—with their robust balance sheets and low commodity exposure—are starting to look like an attractive hedge if the sell-off overextends.

- The Bottom Line: Short-term traders should keep their eyes on WTI Crude and the 10-year yield. Long-term investors must decide if the GTC narrative is powerful enough to pierce through the macroeconomic headwinds.