The SaaS Day of Reckoning: Snowflake, Palantir, and the Crucial Tri-Layer Software Realignment in the AI Era

AI is forcing a brutal tri-layer realignment in software. Data infrastructure giants like Snowflake and Palantir are seeing a massive market re-rating as the "new oil" refineries, while legacy UI-based SaaS platforms face severe disintermediation in the era of Agentic AI.

The global technology sector just witnessed what can only be described as a corporate "Day of Reckoning."

For the past year, capital markets treated the broader software and SaaS sectors with uniform skepticism. The pervasive market narrative—fueled by the explosive rise of large language models (LLMs) from the likes of OpenAI and Anthropic—was that generative AI would completely devour traditional software. Investors feared a brutal "disintermediation" wave: if an AI agent can execute workflows natively, why would an enterprise continue paying premium seat-licenses for legacy application software?

This fear triggered a massive, indiscriminate sell-off—or as Wedbush’s Dan Ives colorfully summarized, "throwing the baby out with the bathwater."

However, the late-May 2026 earnings cycle shattered this monolithic bias. The latest financial data points to a violent structural divergence within tech. While legacy CRM and communication platforms continue to languish in structural gridlock, infrastructure players like Snowflake (NYSE: SNOW) and Palantir (NYSE: PLTR) have staged a ferocious, high-volume counter-offensive.

To understand where the real value will accrue in this next macro cycle, we must unpack the hard data behind Snowflake’s blow-out quarter and evaluate the structural tri-layer realignment reshaping the software landscape.

1. Deconstructing the Snowflake Surge: The Hard Numbers

On May 27, 2026, Snowflake reported its fiscal Q1 2027 earnings, completely subverting the bearish consensus. The stock responded with an extraordinary 34% to 36% single-day surge, jumping from a pre-earnings baseline of roughly $177 to close at $239.15 on May 28—nearly doubling from its cyclical low of $118 printed just weeks prior on April 10, 2026.

Snowflake (SNOW) Cyclical Rebound (Spring 2026)

| Date | Price | Event |

|---|---|---|

| April 10, 2026 | $118.00 | Cyclical Low (Indiscriminate SaaS Sell-off) |

| May 26, 2026 | $177.60 | Pre-Earnings Baseline |

| May 28, 2026 | $239.15 | Post-Earnings Surge (Q1 Blockbuster) |

The fundamental catalyst behind this re-rating lies in an across-the-board operational beat:

- Top-Line Velocity: Total quarterly revenue reached $1.39 billion (up 33% YoY), driven by $1.33 billion in core Product Revenue (up 34% YoY).

- Enterprise Elasticity: Net Revenue Retention (NRR) printed at a historic 126%, indicating that existing enterprise clients are aggressively expanding their ecosystem footprints rather than scaling back.

- Whale Adoption: Large enterprise accounts generating over $1 million in annualized product revenue surged 29% YoY to 779 clients.

- RPO Acceleration: Remaining Performance Obligations (RPO)—representing contracted but unrecognized future revenue—grew by a massive 38% to $9.2 billion, cementing mid-term demand visibility.

Crucially, management aggressively hoisted its forward guidance. Full-year product revenue guidance was revised upward by $200 million—from $5.6 billion to $5.8 billion (representing 31% annual growth)—while full-year operating margins were bumped from 12.5% to 13.5%. Adjusted free cash flow margin climbed 2.1 percentage points to 19.1%, soundly dismantling the thesis that AI adoption would dilute software margins through unrecoverable compute overhead.

2. The Micro-Catalysts: Pipelines, Compute, and Operating Systems

Beyond standard accounting metrics, Snowflake's report highlighted two pivotal micro-catalysts that fundamentally redefined its market valuation.

The $6 Billion AWS Mega-Alliance

Snowflake finalized a massive 5-year, $6 billion strategic expansion agreement with Amazon Web Services (AWS). This is not a standard vendor-purchasing contract; it is a structural symbiosis.

By locking in advanced AWS compute infrastructure and custom AI silicon, Snowflake has successfully insulated its enterprise client base from the global compute bottleneck. The partnership explicitly aims to accelerate the deployment of corporate Agentic AI workloads, linking AWS's underlying raw compute power directly to Snowflake's high-integrity data environments.

Data as the "New Oil" and the Rise of the AI OS

In institutional circles, the consensus is hardening: Data is the new oil, and the data warehouse is the refinery. Enterprise LLM deployment is entirely dependent on clean, compliant, and highly secure corporate data.

Snowflake proved it is monetizing this reality. Over 13,600 enterprise accounts are actively utilizing Snowflake Intelligence capabilities, and more than 7,100 accounts are running native AI code executions. Furthermore, its tactical acquisition of Natoma marks a critical evolution: Snowflake is transitioning from a passive data repository into an AI Agent Operating System.

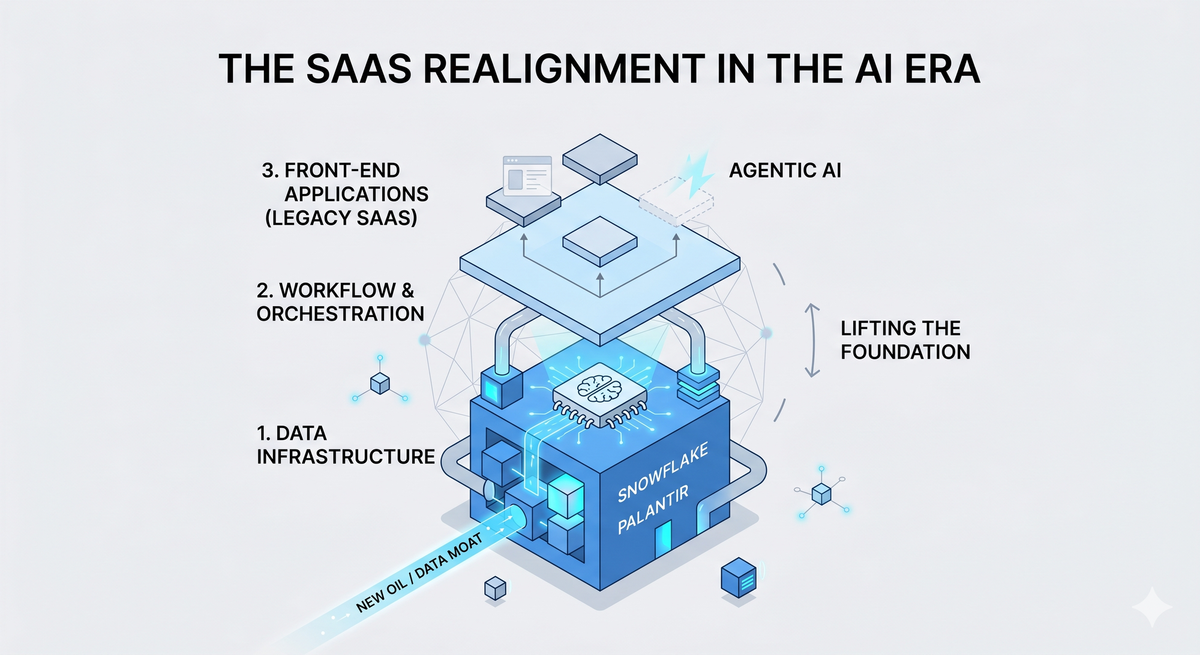

3. The Grand Realignment: The Three Layers of AI SaaS

The market's reaction—rewarding Snowflake with a massive re-rating (driving Wall Street consensus price targets up to $280, with maximum institutional targets touching $400) while hammering legacy players like Salesforce (CRM)—reveals a strict architectural hierarchy.

As corporate IT budgets structurally tilt toward AI, the software ecosystem is bifurcating into three distinct layers, each governed by an entirely different valuation multiple:

Layer 1: Data Infrastructure (The "AI Toll Collectors")

- Core Players: Snowflake, Palantir, Datadog, Oracle.

- The Macro Dynamic: These are the indispensable "water sellers" of the AI gold rush. Because an LLM is only as effective as the proprietary data fed into it, enterprise capital expenditure must flow into data governance, data lakes, and security infrastructure before a single foundational model can be deployed.

- Market Verdict: Strong Bullish Re-Rating. Palantir’s concurrent 7% single-day pop—its largest single-day advance since late 2025—confirms that capital is aggressively rotating back into asset classes with insurmountable, sovereign-grade data moats.

Layer 2: Workflow & Orchestration Platforms

- The Macro Dynamic: These platforms focus on embedding deep, highly customized corporate operational logic. Because swapping out core middleware risks severe operational disruption, these entities enjoy strong customer retention.

- Market Verdict: Neutral to Mildly Bullish. AI acts primarily as an efficiency multiplier and average contract value (ACV) lifter here, rather than a vector for explosive exponential scale.

Layer 3: Front-End Vertical Applications

- The Macro Dynamic: This layer relies heavily on manual workflows and seat-based licensing models. It is highly vulnerable to disintermediation. When autonomous AI agents can natively manage sales pipelines, execute customer support, or generate code, the value of a bloated, seat-licensed user interface collapses. Furthermore, corporate IT budgets are actively being diverted away from front-end SaaS to fund Layer 1 infrastructure.

- Market Verdict: Structural De-rating. Legacy application giants are finding that their AI product announcements generate substantial marketing noise but negligible core revenue acceleration, resulting in compressed cash-flow multiples and compressed valuations.

The BBX Macro Takeaway

The investment thesis for the remainder of 2026 has fundamentally shifted. The era of buying "generic cloud growth" or undisciplined SaaS baskets is over.

The software market has successfully separated structural value from cyclical noise. Growth is no longer being measured by how many user seats an enterprise can capture, but by how much mission-critical data an architecture controls.

As we position across global equities, digital assets, and next-generation Web3 market structures, the lesson of the late-May tech realignment is clear: In an era dominated by algorithmic intelligence, the entity that commands the data infrastructure commands the economics of the entire ecosystem.

Disclaimer: The information, analysis, and opinions expressed in this article are for educational and informational purposes only and do not constitute financial, investment, or trading advice. BBX Research and its authors are not registered financial advisors and do not provide personalized investment recommendations. Market conditions, software valuations, and macroeconomic trends are highly volatile and subject to rapid change. Past performance of any asset or security is not indicative of future results. Always conduct your own rigorous due diligence and consult with a licensed financial professional before making any investment decisions.